The IT services and software engineering sector has been falling since 2022. Indiscriminately. From large caps down to small caps like Nagarro. The punishment draws no distinction — not in size, not in quality.

But one thing the market overlooks is worth stating plainly. Most of these companies aren’t shrinking: they’re decelerating. They went from growing at high double digits (+20% or more) in 2020-21 to high single digits (5-9%). It’s a slowdown in pace, not a contraction.

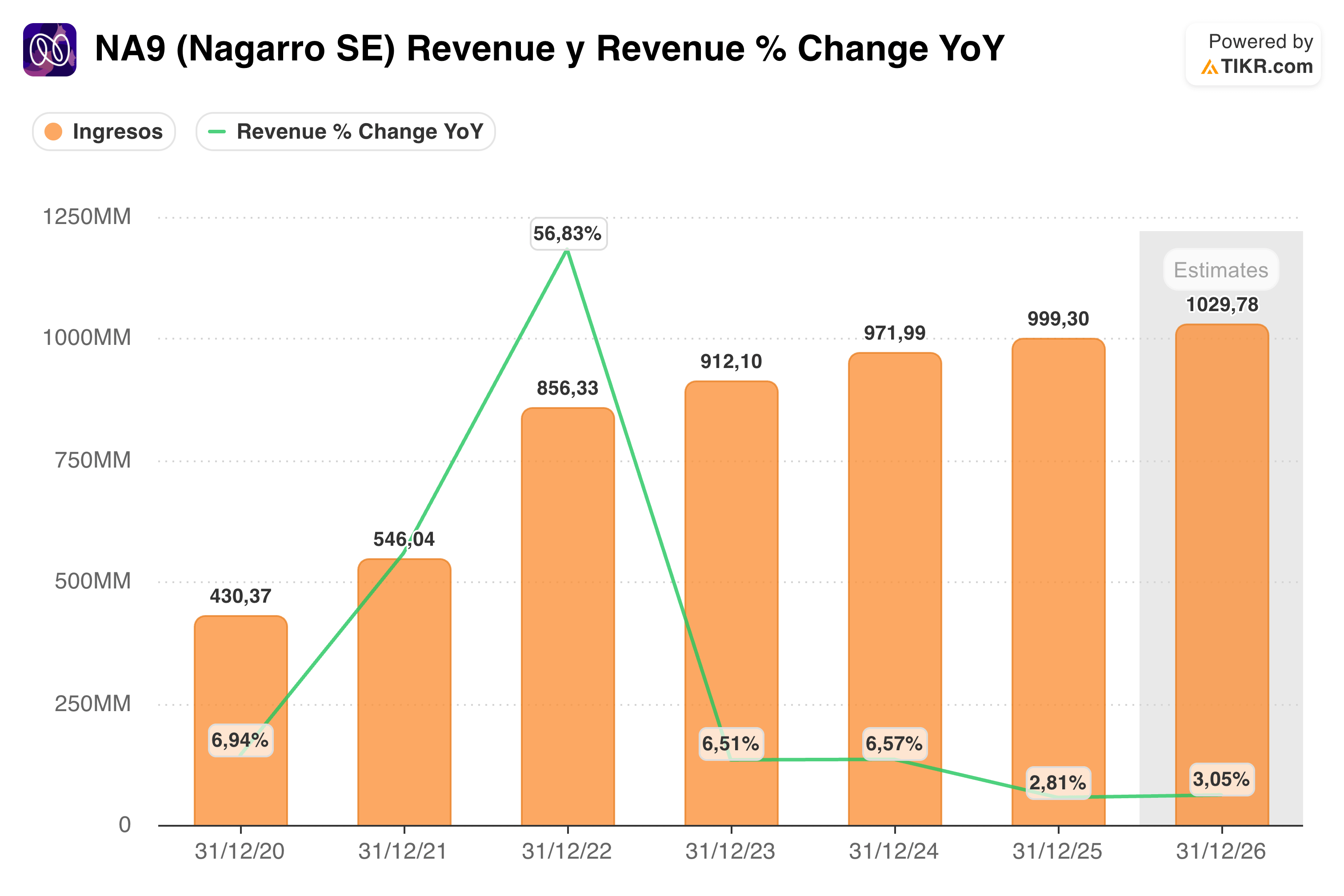

Nagarro is one example. It went from 56% growth in 2022 to 6.1% in constant currency in 2025. For this year, guidance points to roughly +5% at the midpoint of the €1,020-1,080M range.

What is happening in the industry?

The obvious answer is AI. The arrival of ever more powerful models has triggered a technological revolution and, with it, enormous uncertainty around these businesses. Investors have justified the slowdown —we insist: slowdown, not collapse— on a single ground: AI. And the reasoning has a surface logic. If AI writes code the way an engineer used to, and Nagarro does exactly that, then Nagarro disappears and its terminal value is zero. From there, the questions pile up. Does the bill-by-the-hour model survive? If software takes less time to build, does the client capture the entire productivity gain? Are prices falling?

Answering these questions takes three things.

First: metrics. We analyzed Nagarro’s numbers in detail in this article to see how AI was affecting the business. Because the numbers reveal much of what is really happening inside the industry and inside each company.

Second: qualitative judgment. The kind you only get from having been inside. I personally spent more than ten years in the sector.

Third: the voice of the insiders. The people running these companies today.

That’s why we spoke with Manas, CEO of Nagarro, a company billing close to €1 billion. On its last earnings call he left a phrase that deserved unpacking: Nagarro is moving from being a “company of engineers” to a “company of AI-driven transformation.” We wanted him to explain it.

And we took the chance to go further. His read on the future of the industry. Its competitive advantages. Whether the business model is changing —and how. And when he thinks the catalyst will arrive that returns the sector to the double-digit growth of a few years ago.

A high-quality, high-value conversation for every investor subscribed to the research. Without further ado, here is the interview.

The Future of IT Services — A Conversation with Nagarro's CEO

Interviewer: Alejandro Guadalajara, Founder & CEO, Quality Value.

Respondent: Manas, CEO, Nagarro.

Estimated reading time: 5 min

1 · AI substitution and terminal value

The most aggressive bearish thesis on the sector has two versions. The extreme one: if AI replaces software engineers, Nagarro’s terminal value tends to zero. The more nuanced, intermediate one: what used to require 10 engineers over 10 months is now delivered with 5 engineers in 5 months, and the client pays half.

How would you dismantle this thesis, what you’re seeing today in pipeline and renewals, and Nagarro’s internal view over the next 3 to 5 years?

The breathless narratives engulfing the IT services sector today ignore the fundamental segmentation of the sector. Roughly speaking, about 25% of IT service spend goes into infrastructure, another 25% goes into managed services or “run”, perhaps 30% goes into systems integration of standard products, 10% is technology consulting, and 10% is digital engineering where Nagarro focuses. Keeping these numbers always in mind helps deconstruct and dispel these narratives, as far as Nagarro is concerned.

You only “run” what has been set up in previous years – standard products or digital engineering solutions – so infrastructure and managed services volumes have a lot of inertia. You may call them resilient or you may call them lethargic; it depends on the velocity of the rest of the sector. On the other hand, digital engineering work can double from one year to next. If there is confidence in the economy and confidence in the technologies at hand, digital engineering volumes can definitely take off! That will never happen for “run” work.

In fact, AI productivity gains in “run” are likely to be far more disruptive than in enterprise-class “build”, which accounts for a lot of the negative sentiment around the sector. Meanwhile, even in “build”, we have started seeing the trend of standard products and systems integration being replaced by custom digital engineering solutions. This can be a huge tailwind.

All this is not theoretical – we meet large client CIOs and CTOs every day and this is the mental model that resonates with them. So we are bullish!

Our QV read: Nagarro's main vertical is digital engineering — building new software, not maintaining what already exists. And it's precisely the building that holds the most growth potential under AI: AI will make it possible to develop more software, of better quality and more tailored. On top of that, as Manas himself explains later, it is the segment least disrupted by AI.

2 · Pricing power and productivity sharing

Connected to the previous point: Are you seeing pricing pressure on renewals and new contracts?

The majority of our business is time and expense, and, no, we are not seeing undue pricing pressure here. Managed services is different, but this is a relatively small part of our revenue.

Our QV read: Manas acknowledges disruption in managed services —software maintenance— but in building, which is Nagarro's focus, the time-and-expense (T&E) model stays intact.

3 · Business model evolution

Are you already seeing a transition in the business model from traditional time-and-materials contracts toward hybrid models — combining people and AI — and outcome-based pricing?

And the key question: is this new mix accretive or dilutive to the sector’s operating margins?

Where we use AI in delivering software, the cost of the AI is mostly being added to the price of the pod or team. This is not disturbing the operating margins unduly in either direction.

Outcome-based pricing has been around for a long time in the form of milestone payments or SLA-based payments. Newer types of outcome-based pricing schemes are largely fantasy at this point, since client procurement, legal and business teams are usually not open to them, especially for large clients.

Our QV read: The cost of AI (the tokens) is already built into the engineer’s hourly rate and doesn’t affect margins. On outcome-based pricing, Manas reminds us it has been around for a long time —something we can corroborate from our own experience— and that, as of today, no alternative models have caught on, simply because clients aren’t open to them.

4 · Third year of demand contraction

Will we see double-digit growth again, or was that a structurally unrepeatable peak? And if it returns, what would be the specific catalyst?

We should definitely see double-digit growth again, at least for digital engineering or its AI equivalent, as explained earlier.

The specific catalyst would be the maturing of AI-based competitive advantage examples in different industries.

Our QV read: Manas sees a return to growth in digital engineering as highly likely, conditional on AI technology settling in and on the solutions now being deployed starting to deliver results. It’s exactly what we’ve been flagging in earlier articles: it takes technological stability, geopolitical stability, and evidence of return on the AI projects under way. When that happens —and in our view it will— software building will take off.

5 · Sector moat in the AI era

What are the real competitive advantages that protect an IT services firm today? What is Nagarro’s specific moat?

Rather than speak about IT services in general, let me speak about digital engineering in particular, because that is relevant for us. In digital engineering, AI will further expand the productivity gap between ordinary and strong engineers. What an opportunity! Nagarro has always prided itself on its engineering.

We don’t run to a pyramid model like a lot of the industry. Our engineering strength, our deep familiarity with client systems and contexts, our affordable price point, and our ability to advise CXOs on AI transformation – all of these come together to form a powerful moat.

We can defend easily the attacks from “above”, that is, from the consulting firms, while leaning into agentic AI to attack “below” into the traditional “run” business of the IT service firms.

Our QV read: AI will widen the gap between good and bad delivery: if anyone can produce software, the difference will lie in the quality of the product. Manas also points to something we've long argued: a cross-functional —not pyramidal— corporate culture brings agility and becomes an advantage over heavily hierarchical organizations. He also mentions price competitiveness, an aspect of Nagarro we've always highlighted: with its labor base offshored in India, at costs below Western levels, it can compete more effectively. Finally, he underscores its ability to deliver end-to-end solutions, from consulting to execution: it reaches where pure consultancies don't execute, and advises where execution firms don't advise.

6 · Capital allocation at trough multiples

Are you evaluating buybacks taking advantage of current price levels?

No comments! We have a new, highly experienced CFO. We are evaluating capital allocation opportunities continuously.

Our QV read: On 17 April, Nagarro announced the appointment of Prateek Aggarwal as CFO, a profile with extensive sector experience (twelve years at HCL Tech). It's logical, then, that the company wants to give him room to define the best possible capital allocation policy. Our full valuation is in the article (here), where we analyze the latest results.